INDOPHIL NICKEL CORRIDOR · DEEP REPORT · WA-2026-07-11

NICKEL-FREESHOCK

Datang EVvsIndonesia's Nickel Gambit

A full-size 7-seater BEV shipped with zero nickel and zero cobalt — while Jakarta's RKAB tap turns from quota cut into a de-facto flood. Two forces converge at LME 16,300.

Datang EV orders

150,000

53 days · RMB 40bn+ · zero Ni · zero Co

LME nickel spot

$16,300 /t

6-month low · June −14% MoM

China LFP install

82%

NMC down to 18% · trend accelerating

Indonesia RKAB 2026

~280 Mt

Cartel logic self-abandoned

PUBLISHED · JUL 11 2026·DEEP REPORT · 6 PANELS·ENGLISH·~14 MIN READ

The shock in one page

Two collisions rewired the nickel narrative in a single quarter: a flagship BEV proved 950 km range with zero nickel, while the country that supplies 70% of global ore quietly unwound its own quota discipline.

Demand shock

Zero Ni

Datang EV — a 7-seater full-size SUV — shipped 150,000 units in 53 days on an LMFP chemistry. The premium BEV segment has now openly rejected the nickel-cobalt cathode as a mandatory ingredient.

Supply shock

+280 Mt

Indonesia's 2026 RKAB additions returned quota headroom well above cartel-consistent levels. What was framed as scarcity discipline in Q1 has become a de-facto flood by mid-year.

Price collision

$16,300

LME nickel printed a 6-month low on July 6 — testing the top-quartile RKEF cash cost curve at $15,800–17,000/t. Any further slide moves marginal Indonesian NPI lines into cash-negative territory.

The read

Neither shock alone would break the nickel bull case. The problem is convergence: demand elasticity for Class-1 nickel is now visibly negative in the fastest-growing BEV segment, at the exact moment supply discipline broke. Cost-curve support becomes the only floor left.

Chronology · Q2 2026

Date

Event

Signal

Apr 18

Indonesia signals additional RKAB tranches to "stabilise supply"

Supply-side pivot

May 08

LME nickel prints May peak at $19,600

Last defence

May 17

Datang EV opens pre-orders — LMFP cathode, 950 km CLTC

Demand shock

Jun 12

Datang EV crosses 100,000 orders in 26 days

Confirmation

Jun 30

China LFP install share prints 82% · NMC 18%

Structural

Jul 06

LME nickel hits 6-month low at $16,300

Collision

Jul 09

Datang EV orders cross 150,000 · RMB 40bn+ notional

Scale

The Datang event · 150,000 orders in 53 days

A price-band shift, not just a product launch. Datang EV lands RMB 150k below premium peers with a chemistry that skips nickel and cobalt entirely — and the order curve confirms the market read it as a mainstream upgrade, not an experiment.

Range · CLTC

950 km

Global full-size BEV record — 0 nickel, 0 cobalt in cathode.

Energy density

210 Wh/kg

LMFP cathode + Si-C anode. Closes ~85% of the NMC premium gap.

Fast charge

10 → 70%

19 min at 5C. Speed replaces range anxiety as the buying axis.

Pack cost

¥580 /kWh

Industry average ≈¥1,000. A 42% pack-cost gap flows straight to sticker price.

Why the order curve matters

150,000 orders in 53 days from an RMB 300k+ segment isn't retail enthusiasm — it's fleet, corporate and premium-family conversion. This is the buyer cohort that historically underwrote NMC's price premium. Their exit is what makes the substitution structural rather than cyclical.

Price positioning · RMB 10K

Model

Cathode

Range CLTC

Starting price

Delta vs Datang

Datang EV (base)

LMFP

820 km

RMB 289k

—

Datang EV (long-range)

LMFP

950 km

RMB 329k

—

Premium NMC peer A

NMC 811

720 km

RMB 458k

+RMB 129k

Premium NMC peer B

NMC 622

680 km

RMB 478k

+RMB 149k

Premium NMC peer C

NMC 811

750 km

RMB 519k

+RMB 190k

CLTC = China Light-duty Test Cycle. Prices are opening-tranche list, exclusive of subsidies and dealer discounts.

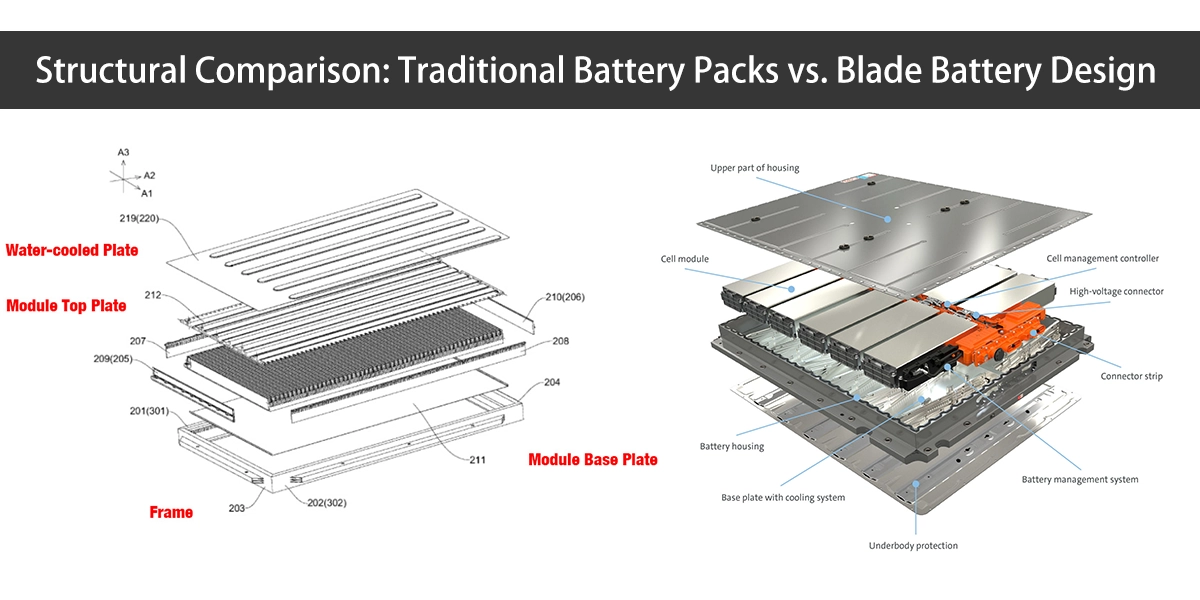

Under the floor · LMFP pack architecture

The Blade-family LMFP pack replaces the module layer entirely — cell-to-pack (CTP) with prismatic long-form cells acting as their own structural members. That is where the nickel savings compound: less inactive mass means less energy per km, means less cathode per km.

Exterior · Launch livery

Full-size 7-seat SUV, 5,263 mm length. Nameplate "大唐" — Chinese for "Great Tang".

Exterior · Side profile

3,050 mm wheelbase enables the low-profile pack floor that hosts the CTP LMFP structure.

Pack architecture

Left: traditional module-based pack with water-cooled plates and separate framing. Right: cell-to-pack layout — cells become structural members.

Cathode chemistry

Iron-phosphate framework with manganese doping (LMFP). Zero nickel, zero cobalt. Thermal runaway threshold ≈ 270°C.

English tour · 2026 BYD Great Tang EV — 950km Range 7-Seater SUV · Full TourOpen on YouTube ↗

Cathode arithmetic · why it hurts nickel

NMC 811 cathode consumes ~0.75 kg of Class-1 nickel per kWh. A 100 kWh Datang pack running LMFP consumes zero. At 150,000 units × 100 kWh, that is 11,250 tonnes of nickel demand deleted in one product cycle. Global Class-1 growth for 2026 was budgeted at ~80 kt — a single model absorbs 14% of that budget in 53 days.

LME nickel · mean reversion toward the cost floor

Spot has retraced the entire post-RKAB rally. Forecasts cluster in a $15,250–17,357 band — every dollar below $16,500 pushes another slice of Indonesian RKEF and Chinese matte-derived NPI capacity into cash-negative operation.

May 8 — May peak at $19,600 · last defence before demand-side news.

Jul 6 — 6-month low at $16,300 · retracement complete.

Forecast band — $15,250 low, $17,357 high.

Cost curve pressure

Indonesia RKEF cash cost · $13,500–15,200 /t Ni (saprolite ore ≥1.6%).

Indonesia HPAL cash cost · $9,800–12,400 /t Ni (limonite feed).

China matte-NPI conversion · $16,800–17,800 /t Ni-equivalent.

Top-quartile RKEF · $15,800–17,000 /t — the price where the marginal RKEF line stops making cash.

The credibility gauge

Indonesia cannot simultaneously (a) cap ore output to defend price, and (b) feed a smelter fleet that now runs on ~330 Mt/yr of appetite. Q2 2026 revealed the choice: feed the smelters. Once made, that choice is hard to reverse — smelter offtake contracts have priority in the political queue.

Nickel demand treemap · global 2026

Demand block

2026 share

Growth vs 2025

Nickel-free exposure

Stainless steel (300-series)

65%

+5.2%

Immune — mechanical property spec

Batteries · NMC/NCA

17%

−12.4%

Directly displaced by LMFP

Alloys · superalloys

11%

+3.1%

Immune — aerospace/energy spec

Plating & other

7%

+1.5%

Immune

Stainless is the base load that keeps the market alive; batteries are where the growth story lived — and where LMFP now bites.

The corridor · where the collision lands

Six Indonesian smelter parks, three Chinese battery hubs, and one automaker campus draw the physical geometry of the shock. When Class-1 nickel demand thins, the pressure travels up the chain toward the RKEF lines closest to price parity.

Indonesian smelter park (RKEF / NPI)HPAL / MHP plant (Class-1 route)China battery / cathode hubOEM automaker campus (Datang)

Outlook · what to watch

Six read-throughs from the shock — the ones that move first, and the ones that move last.

1 · Class-1 vs Class-2 spread

The Class-1 premium over Class-2 (NPI) is the market's most direct thermometer of battery-nickel demand. A spread compression below $2,500/t confirms the LMFP read-through is priced in.

2 · Marginal RKEF idling

First to cut are non-integrated RKEF lines in Sulawesi Selatan without captive ore. Watch for July–September utilisation prints below 75%.

3 · HPAL / MHP resilience

HPAL cost curve sits far below RKEF. HPAL operators absorb pain later — but their Class-1 output is precisely what LMFP no longer needs.

4 · China NMC producer response

Watch for NMC-heavy cathode producers publicly announcing LMFP capacity conversion. This is the moment the substitution becomes structural in supply capex.

5 · Indonesia RKAB re-tightening

Political pressure to defend price will return. Any RKAB re-tightening announcement without smelter offtake unwind is theatre — read it accordingly.

6 · Copper/nickel substitution reversal

The offset is copper — LMFP packs use ~35% more copper per kWh. Nickel's loss is partly copper's gain, and cathode-conversion capex will follow.

Bottom line

The nickel bull case rested on a single assumption: that battery-grade demand would keep growing faster than Indonesia could supply. Datang EV proved the demand-side assumption is falsifiable at scale, and Indonesia proved the supply-side assumption is politically fragile. What's left is a stainless-driven market with a cost-curve floor — a very different asset than the one that traded to $30,000/t in 2022.

◆ By Invitation Only

Get inside the Nickel Corridor

Live corridor map, twice-weekly briefings, deep reports, and the shipper & permit database used by miners, smelters, cathode makers, banks and OEMs across the IndoPhil corridor.